Managing Your 401k Part 3

Do you lack time for or interest in planning your portfolio holdings in more detail? Or have you been putting off investing in the markets altogether? Balanced and target date funds help simplify the investment process by delegating many decisions to the fund manager, from portfolio construction to subsequent rebalancing. But this simplification is not without disadvantages.

“Balanced and target date funds help simplify the investment process by delegating many decisions to the fund manager.”

Balanced funds can be a great way to begin investing with a minimum amount of cash. Starting early adds time your portfolio vitally needs to grow, allowing you more freedom in achieving your goals. The fund manager automatically maintains your asset mix so that you never have to rebalance the fund.

In this last article of our three-part series on Managing Your 401k, we focus on balanced and target date funds which have become increasingly available in retirement plans.

- Balanced funds explained

- Target date funds explained

- Using balanced and target date funds

- Concluding thoughts

Balanced Funds Explained

Considered a “one fund option”, balanced funds combine securities from more than one asset class, typically equities (stocks) and fixed income (bonds). Owning securities across multiple asset classes is what differentiates a balanced funds from those which are asset class or sector specific, like US large cap or technology stocks.

“What if your balanced fund could automatically adjust more conservatively as your portfolio’s target date approaches?”

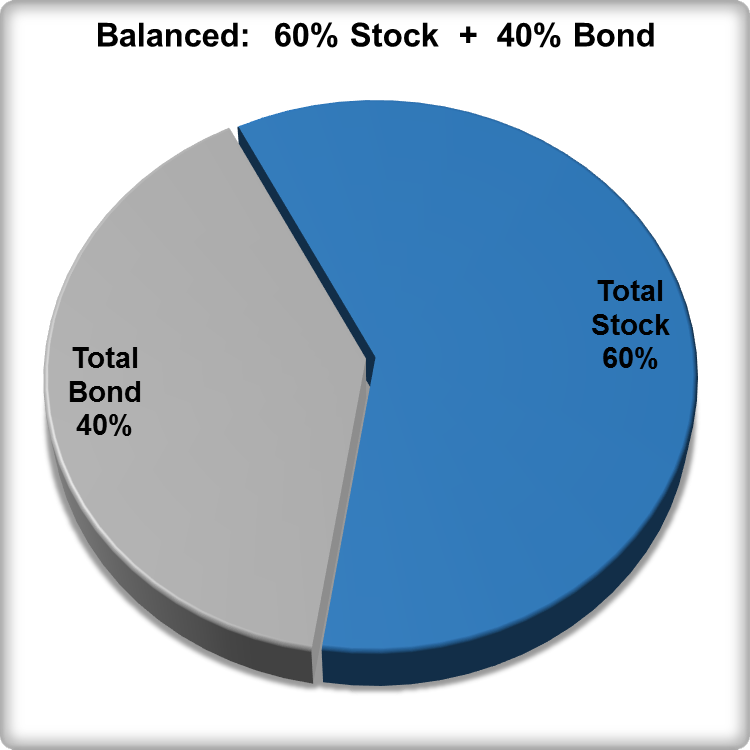

Traditional balanced funds typically maintain a fixed proportion of each asset class over time. A moderately allocated balanced fund may hold 60% of its assets in stocks, and the remaining 40% in bonds, a “60/40” mix or asset allocation. The fund’s prospective sets boundaries for what the portfolio manager may hold and how much.

A balanced fund may be composed of individual securities, or entirely of other funds. Vanguard’s Balanced Index Fund1 holds about 3,000 individual US stocks and bonds. US stocks like Apple Inc. comprise 60% of the fund’s assets. The remaining 40% is invested in individual bonds such as Harris Corp’s 2.7% coupon bond maturing April 2020. Vanguard’s STAR Fund is also a 60/40 balanced fund, but composed entirely of actively managed Vanguard funds, known as a “fund of funds”.

Target Date Funds Explained

Instead of maintaining a static asset allocation, what if your balanced fund could automatically adjust more conservatively as your portfolio’s target date approaches? A “target date fund” (TDF for short)2 does just that! It is a special type of balanced fund designed to systematically decrease stock exposure over time. TDFs are usually funds of funds having two key elements:

- The glide path: how the asset allocation changes over time

- The target date: a reference date to which the glide path is positioned

The Glide Path:

Glide path or glideslope refers to how the asset allocation of the fund transitions over time, from a relatively high exposure to stocks, to its most conservative allocation maintained for the remaining life of the fund. Glide paths vary between fund families in equity exposure, transition time, and target date positioning. Assumptions also vary and may include that an investor maintains a “reasonable savings rate” up to the target date, withdrawing thereafter over a “moderate” time horizon. These affect outcome probabilities and in turn glide path design.

“A portfolio’s intended purpose drives selection per glide path design and transition end date.”

Figure-1 describes the 32-year glide path3 of Vanguard’s “target retirement” family of funds. The transition period begins 25-years before the stated target date, declining gradually from 90% equity exposure to about 50% on the target date. The transition ends seven years later, maintaining 30% equity exposure thereafter.

Much has been made about where the target date is set relative to the glide path. Classifying funds as to-funds or through-funds is altogether irrelevant. A portfolio’s intended purpose drives selection per glide path design and transition end date.

The Target Date:

The target date is simply a reference point relative to the glide path’s transition period. Funds intended for retirement accounts usually position the target date several years before the end of the transition. Placement is driven by standardized assumptions of longevity, based on retiring at 65-years of age.

“You do not have to invest in a target date fund which matches your retirement date.”

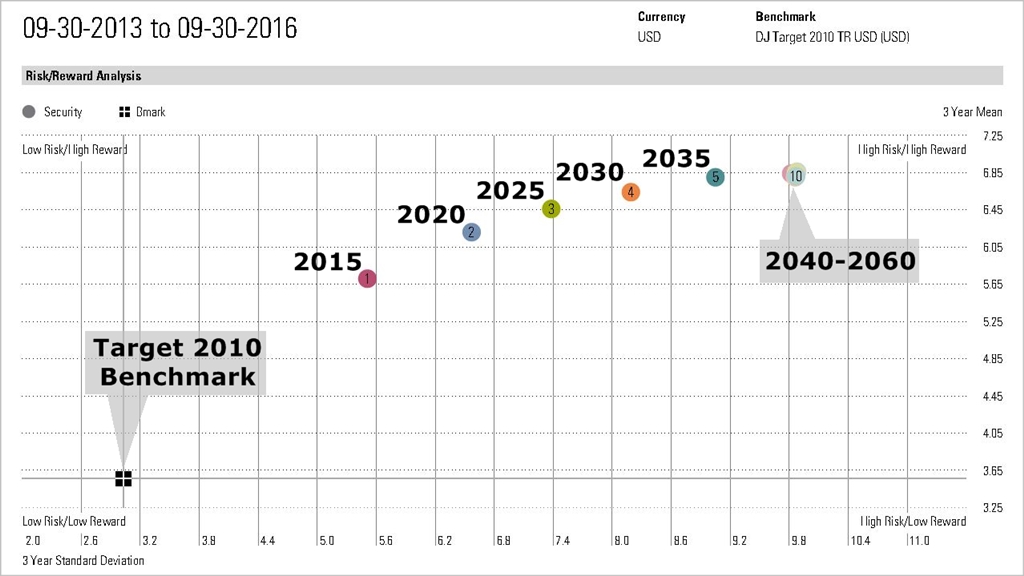

For illustrative purposes, figure-2 plots the risk/reward4 characters of one family of TDFs having a 25-year transition to the target date, and continuing seven more years before becoming fully conservative. Risk is plotted on the horizontal axis in the form of annualized volatility, increasing from left to right. Reward is plotted on the vertical axis in the form of average annualized total return. Results will vary with market conditions, asset composition and glide path design.

Funds dated 2045-2060 appear to be performing the same. They all have the same allocation and composition, not yet having started their transition. Meanwhile, funds dated from 2015 through 2040 are all in some phase of their transition. The 2015 fund is 6-years away from becoming as conservative as a 2010 fund which is now essentially a static, conservatively allocated balanced fund.

Using Balanced and Target Date Funds

Let’s discuss a few considerations when using balanced or target date funds.

You do not have to invest in a TDF which matches your retirement date. Using an earlier (later) target date produces a more conservative (aggressive) trajectory. For a college savings account, a transition period ending before withdrawal may be more appropriate, regardless of the stated target date.

“Ultimately, a one-fund-solution may not be the best answer for YOU!”

What if your plan offers a static 60/40 balanced fund, but you need a 70% equity allocation? You can create the equivalent by buying 75% in the balanced fund, and 25% in a diversified stock fund. Switching to a bond fund creates a 45% equity portfolio. The downside is that any rebalancing5 is left to you.

Caveats:

Ultimately, a one-fund-solution may not be the best answer for YOU! They are rigid in their approach, with disadvantages common to one-size-fits-all solutions. Imagine a store selling only green shoes in size-9.

- TDFs make general assumptions which may not be suited to your specific situation.

- A fund may forgo less traditional asset classes such as REITs, precious metals, and commodities, rendering your portfolio under-diversified.

- Management may be unable or unwilling to make tactical adjustments such as decreasing effective duration during rising interest rate environments.

- Loss of control: What happens in times of extended bull and bear markets like those since 2000?

Not all funds are alike and it pays to look under the hood, examining actually holdings and investment methodology.

Concluding Thoughts

Markets change, sometimes suddenly and dramatically. At Coherent, we prefer a more hands-on approach over a “set it and forget it” investment philosophy. We manage a variety of highly diversified, customizable, balanced strategies. We adjust portfolios dynamically using a systematic, disciplined methodology with a sensitivity to impending market conditions.

We feel this is the best approach. It doesn’t have to be right for everyone, just for you.

I hope the insights shared in this Managing Your 401k series have opened up possibilities for managing your own investments. Feel free to contact us whether you have questions, want a second opinion, or would like help in designing your retirement plan allocation.

Warm regards,

Sargon Zia, CFA

December 28, 2016

You are welcome to comment!

Recommended reading:

Managing Your 401k Part 1

Managing Your 401k Part 2

Footnotes:

- The Vanguard Group, www.vanguard.com, November 30, 2016

- Target date funds come in many names depending on the fund family including lifecycle, life style, target retirement, and age-based funds.

- Source: https://retirementplans.vanguard.com /ekit/pmed /tdic/images/2_0 /Glide_Path_Web_2015_RGB.png

- The information contained herein: (1) is proprietary to Morningstar and/or its information providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its information providers are responsible for any investment decisions, damages or losses arising from any use of this information or any information provided in conjunction with it. This report is for information purposes only, and should not be considered a solicitation to buy or sell any security. Past performance is no guarantee of future results.

- Rebalancing to a static allocation triggered by an arbitrary tolerance range works best in only the most ideal sideways market swings in both distance and time – an ironic strategy of choice for the “we don’t time the market” crowd. It is convenient for tracking (at best) a static benchmark. In contrast, buy-and-hold and a constant proportion rebalancing strategy both outperform in persistent market trends as have existed since the year 2000.