Money for Nothing Checks for Free

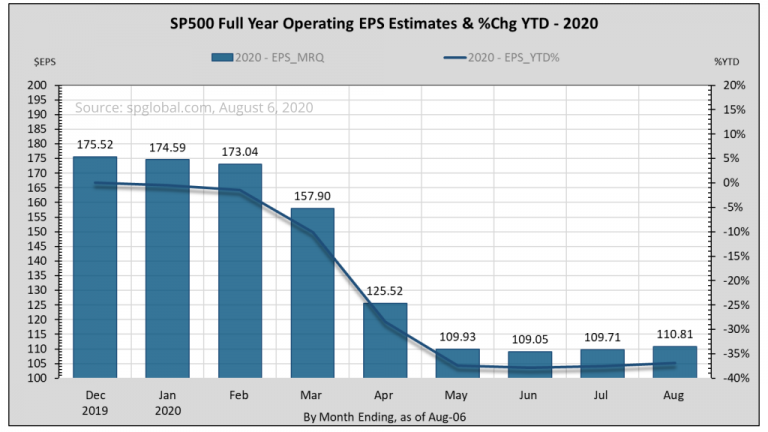

While our once vibrant economy has been quarantined for state-mandated experiments, earnings outlook is beginning to stabilize for a path to recovery. It isn’t pretty.

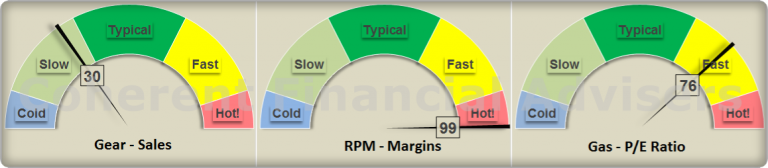

While our once vibrant economy has been quarantined for state-mandated experiments, earnings outlook is beginning to stabilize for a path to recovery. It isn’t pretty.

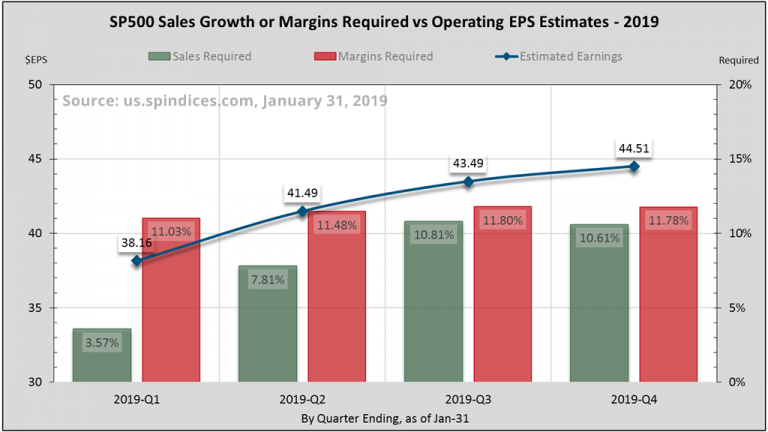

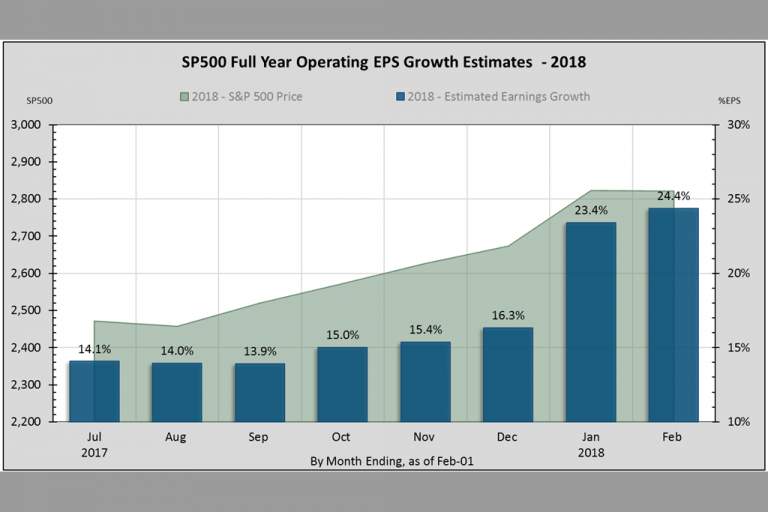

Earnings growth set a new millennium record in 2018. It’s now a major hurdle to growth in 2019. Growth estimates are a third of last year’s and declining. The mortar in the market’s wall of worry now is margins.

Earnings continue their record-breaking trend. S&P 500 price gains have been driven by earnings growth as overall valuation has subsided. Record margin levels contributed half the earnings growth, but may be the main drag in 2019.

Stock market’s character has fundamentally shifted. Gains last year came almost entirely from earnings, and at the lowest volatility in three decades. Earnings growth is at a seven-year high. But future growth depends on margins already at nose-bleed levels.

Earnings in 2017 have been spectacular. Estimates for 2018 have risen to a millennium record, and so have market valuations. But high margins levels caution for more reasonable expectations. The recent correction may just be an omen.

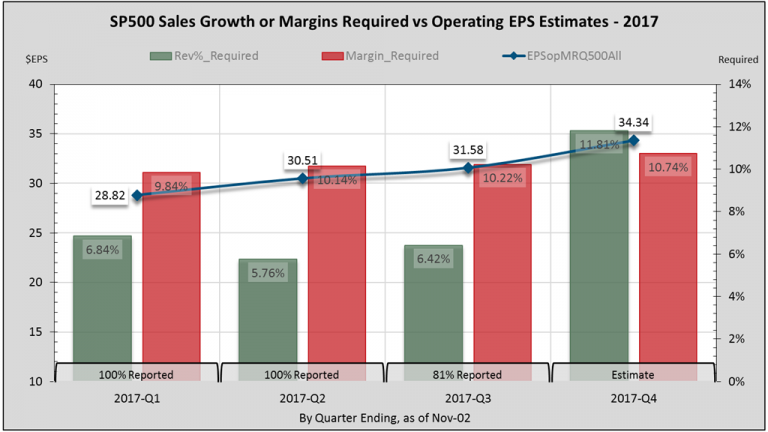

With third quarter reporting nearly concluded, S&P 500 companies are delivering growth rivaling post-recession 2010. Not surprisingly, valuations are also breaking records. Meanwhile, record margins present more challenging hurdles to 2018 growth.

On August 21, the Great American Solar Eclipse will trace a “path of totality” across the continental United States. Allegorically, expectations of accelerated earnings growth may become eclipsed by looming comparable earnings hurdles at already elevated stock market valuations.

Companies are finally turning performance from “worst-since” to “best-since” while wrestling rising hurdles in a radically changing environment. Expectations have risen to over 20% growth, much of which markets have priced-in at peril of a more serious correction.

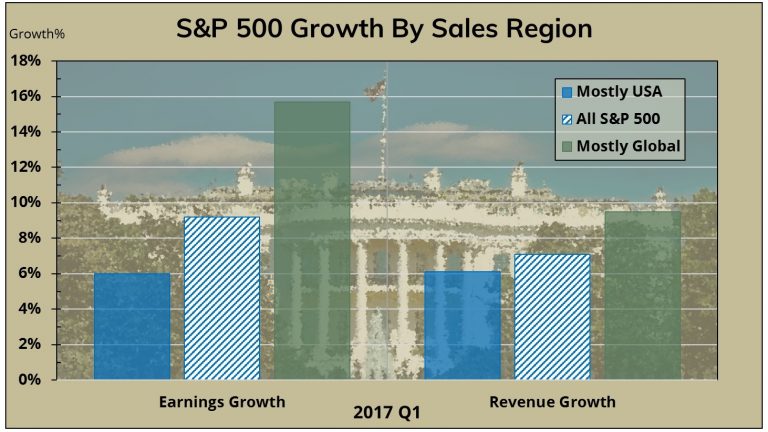

US companies face unrealistically high expectations for 2017 earnings growth, while contending with stock prices which have jumped ahead to record levels. Markets don’t react well when priced-in expectations disappoint.

In earlier articles, I introduced the “silver lining for 2016.” The further 2015 earnings declined, the lower the bar became for realizing a positive 2016 earnings growth rate. Third quarter earnings look to become the first growth we have seen in nearly two years. This silver lining has finally arrived, but not without its caveats.