Coherent Investor June 2016

The Fed just released their decision on short term interest rates after the fourth of eight such meetings scheduled for this year. Will the Fed raise short-term rates this year? How have their decisions affected stock and bond markets? Get ready for some objective answers.

The salient question is, “What does the market think The Fed will do?” Market participants move prices when they act on what they believe. As investors, you and I are paid by the market’s movement, not commentator opinion.

“Opinions are usually wrong. The market by definition is always right – it pays the investor!”

One of the research studies we have designed at Coherent addresses topics related to The Fed Funds rate. We analyze the data to determine the market’s collective opinion on rates, and its effect on other market segments such as stocks and bonds.

In this article we use the 30-Day Federal Funds Futures contract to address these questions.

- Will The Fed raise the short-term interest rate this year?

- How are stock and bond markets affected by Fed Rate decisions?

The challenge in answering important questions is to first properly word them. Once irrelevant and subjective forms have been eliminated, the real question can be addressed more accurately and objectively.

Will The Fed Raise The Short-Term Interest Rate This Year?

There are three forms of this question, two irrelevant, and one salient.

- Irrelevant question #1: “Will The Fed raise rates?” I don’t know. Chair Yellen has yet to invite me to her meetings. The Fed itself may not know at this time.

- Irrelevant question #2: “Do you think The Fed will raise rates?” What I say or do does not move the market so it doesn’t matter what I think. The same goes for most of the talking heads on TV.

Which brings us to the salient question…

“Does the market believe The Fed will raise rates this year?”

As investors, you and I are paid by the market’s movement. Opinions are usually wrong. The market by definition is always right – it pays the investor.

The 30-day Federal Funds Futures market is an objective aggregator of what the market really thinks The Fed will do. It is where market movers act on their beliefs with real money. Contracts are cash settled against the average daily Fed Funds overnight rate for the specific delivery month1.

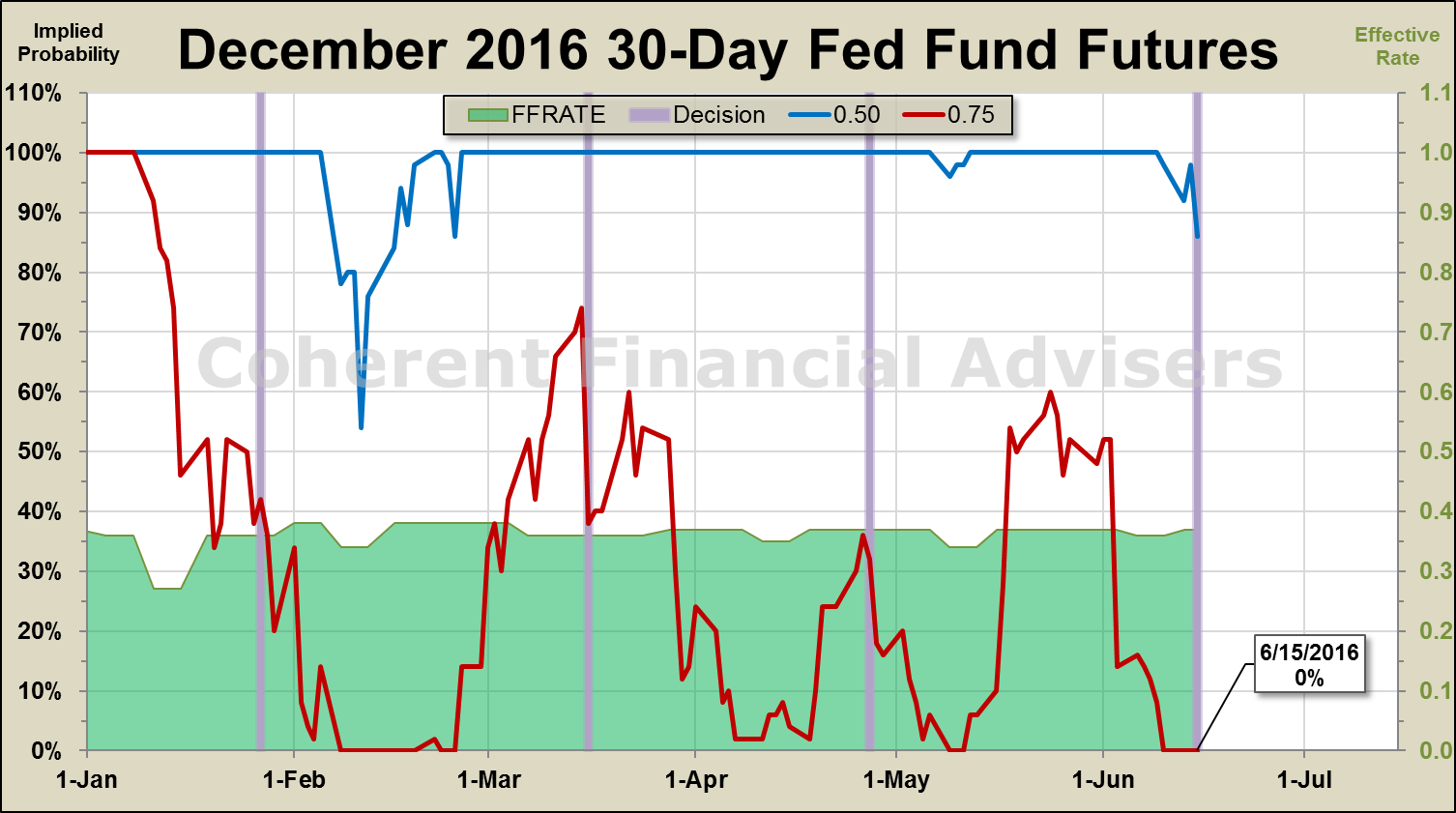

Using the December 2016 contract’s price data, the chart in figure-1 illustrates the approximate probability2 the market attributes to a series of target Fed Funds rate increases by year’s end. The blue line traces the probability of a rate hike from 25bps to 50bps (0.50% or 50-basis points), and the red line from 50bps to 75bps. The vertical purple lines mark FOMC3 rate decision meetings. The green area is the effective rate, currently 37bps4.

At the start of this year, the market attributed a 100% probability of two rate hikes to 75bps by year end. During the sharp market selloff through mid-February, the probability of even one rate hike this year fell to 54%. Subsequent signs of possible economic improvement raised the probability of a second rate hike to 74%, until the March and April rate decisions reduced that outlook to zero.

At this time, the market is betting on an 86% chance of one rate hike to 50bps.

How Fed Funds Futures Rate Affects Bond Markets

The bond market as represented by the yield on the 10-year US Treasury Note Index has reacted as one might expect. When the perceived probability of a rate hike increases, the 10-year note rate is expected to rise. However, the magnitude and explanatory power of the relationship fluctuates over time and with market conditions.

Our research indicates that year to date, the 10-year yield has changed on average about 11bps for every 10bps change in the Fed Funds Futures rate. Changes in Fed Funds rate have explained on average about 60-80% of the corresponding changes in the 10-year yield.

How Fed Funds Futures Rate Affects Stock Markets

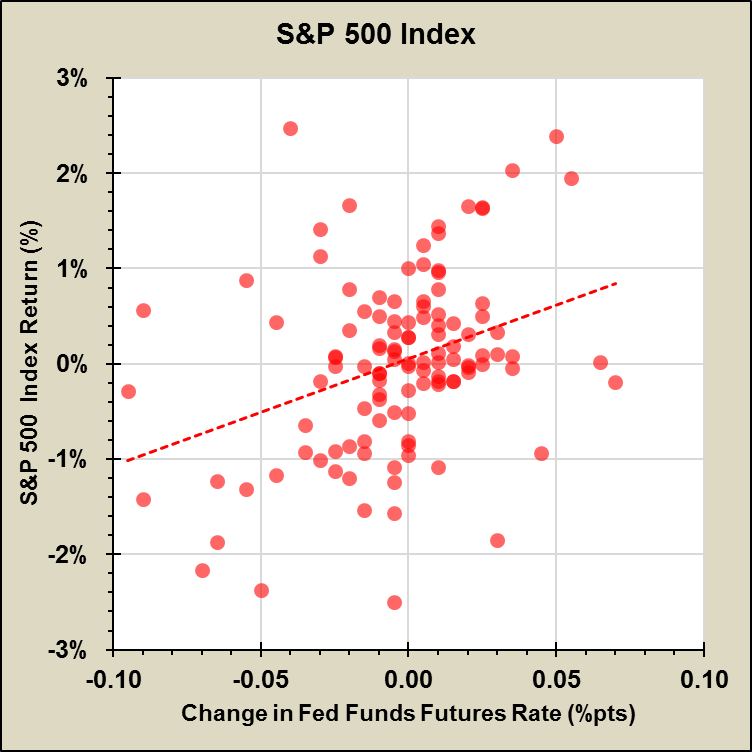

In general, one would anticipate stocks to respond negatively to the prospect of rising interest rates. The relationship between stocks and changes in the Fed Funds rate can vary drastically both in magnitude and direction, depending in part on where we are in the overall business cycle.

Year to date, the relationship between stock market returns as represented by the return on the S&P 500 Price Index, and Fed Funds Futures rate has been very weak. This can be seen in the scatter plot (figure-3), especially when compared to that of the 10-year note (figure-2).

In terms of explanatory power, a change in Fed Funds rate explains on average only about 12-28% of the change in S&P returns. The effect fluctuates over time, increasing in strength around Fed decision dates.

Market Movement Explained By Fed Funds Futures

The chart in figure-4 is another way to view the effect of the Fed Funds Futures rate on stocks and bonds. The weekly period is a better interval of measure than daily, but I have provided both studies.

The chart on the left shows that year to date, 60% of the daily change in 10-year bond yields can be “explained” by changes in the Fed Funds Futures rate. Meanwhile, the rate only explains 12% of the daily return on the S&P. The remainder is due to market factors other than the Fed Funds Futures rate.

Changes in the Federal Funds Futures rate itself may not necessarily cause changes in bonds or stocks. What we are measuring here is simply a correlation. Causes may be due to factors mutually shared by the Fed Funds rate, the 10-year note, and the stock market, such as inflation pressures.

No Surprises

Since the Bernanke-Fed declared glasnost, The Fed Chair and other members of the Board of Governors have offered their opinion plainly and openly on economic conditions and monetary policy. The bulk of The Fed’s rationale is provided in speeches and publications in addition to the usual rate decision press releases often the focus of the media. The market’s take on the direction of interest rate policy changed little after The Fed’s rate decision today, a testament to The Fed’s openness.

If you have any questions or comments, we would be delighted to hear from you.

Warm regards,

Sargon Zia, CFA

June 15, 2016

You are welcome to comment!

Published regularly, the Coherent Investor series focuses on the current conditions of the securities markets as interpreted by the author and Chief Investment Officer of Coherent Financial Advisers, unifying multiple investment disciplines including fundamental and technical analysis.

Footnotes:

- See CME Group 30-Day Federal Funds Futures Contract Specs, www.cmegroup.com/trading/interest-rates/stir/30-day-federal-fund_contract_specifications.html

- There are many ways to calculate Fed Funds rate probability and no process is an exact science let alone a perfect predictor. At Coherent we have devised a simplified yet effective approach based on the work of Terrill R. Keasler and Delbert C. Goff. See also www.economics-finance.org/jefe/fin/KeaslerGoffpaper.pdf

- The target federal funds rate is set by the Federal Open Market Committee or FOMC, the monetary policymaking body of the Federal Reserve System. Composed of 12 members, the FOMC delegates responsibility for implementing U.S. monetary policy, including the effective federal funds rate, to the Federal Reserve Bank of New York through its open market operations. See also www.newyorkfed.org/aboutthefed/fedpoint/fed32.html

- Data sources: Effective Fed Funds rate from the Federal Reserve Bank of St. Louis database. Futures data from the CME Group. S&P 500 and 10-yr Note Index data from Yahoo Finance. Analysis and presentation of this data produced by Coherent Financial Advisers, LLC.