Manager’s Letter 2014 Q3

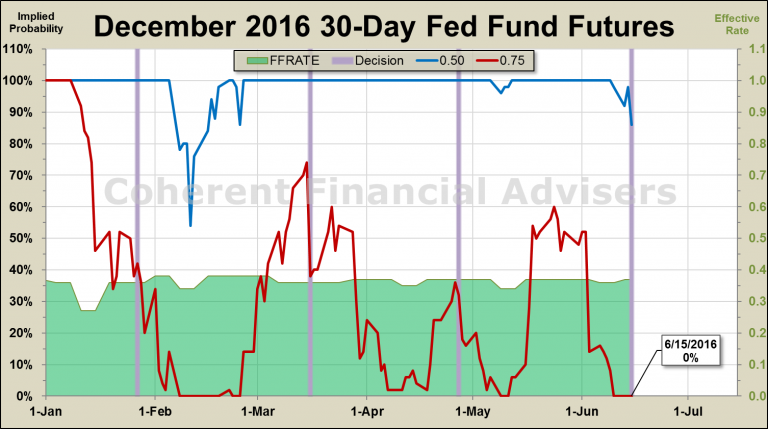

You’ve often heard me say that I manage risk rather than return. I view risk in two categories: (1) being aggressive and risk a market decline, or (2) being defensive and possibly miss a market rally. Recently we’ve been doing some managing of the second kind. Below is a picture of the “why”.

The left chart is from the previous quarter’s letter, updated through October 6. The chart describes the S&P 500 Index moving to new highs while individual stock participation dropped off. Participation is my word for “breadth”, a measure of the price action of individual stocks relative to their aggregate index. When the S&P made new highs in September, several measures of breadth worsened together, prompting defensive action.

The right chart is a close-up of the S&P since August 1 illustrating three times we’ve reduced equity exposure: September 16, 19, and October 3. (#1) For the first time this year, equity allocation in mutual fund portfolios was reduced in favor of fixed income. (#2) ETF & individual stock portfolios received options which hedged 15% equity allocations through October 1. (#3) Physical equity allocations were reduced in ETF & individual stock portfolios.

Warm Regards,

Sargon Zia, CFA

October 6, 2014

Note to reader: Published quarterly, the Manager’s Letter series primarily communicates the author and Chief Investment Officer’s personal opinion on the markets. This article was originally written in October of 2015 and is provided to offer continuity and context for future articles.