Manager’s Letter 2017 Q1

The beautiful daughter of a deceased physician, Helena reasons with the skeptical King to allow her to treat his terminal illness. She wins him over saying, “Oft expectation fails, and most oft there where most it promises; and oft it hits where hope is coldest, and despair most fits.” From Shakespeare’s play, All’s Well That Ends Well, these words aptly describe investor psychology at market peaks and troughs.

“Today’s market promises most, a place where expectation often fails.”

When rallies become extended, so do expectations as the best probable outcomes are priced-in. Conversely, in protracted corrections, “hope is coldest” as the worst probable outcomes are discounted. Today’s market promises most, a place where expectation often fails.

Promises

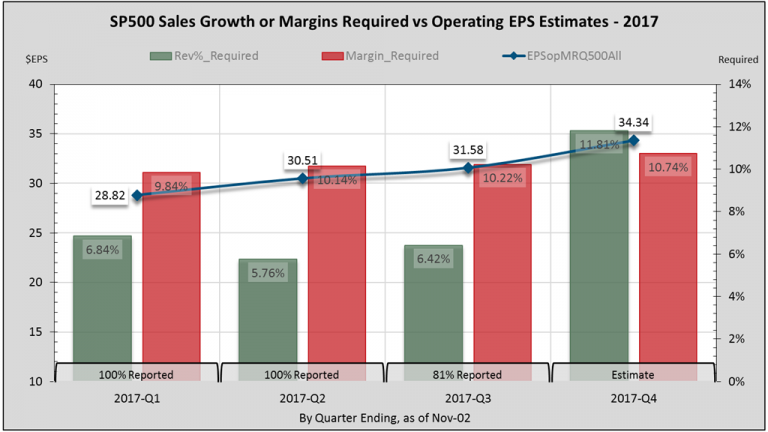

The S&P 500 Index is priced (PE) about 18-times full 2017 operating earnings which are estimated to grow 22% as the first chart shows. That’s rich if these expectations were modest. They’re not. Operating earnings last year were estimated to grow 20%. They’ve turned out less than 6%. I know, this time it’s different. But human nature isn’t, and S&P companies will need to deliver a combined 22% growth from sales or margins.

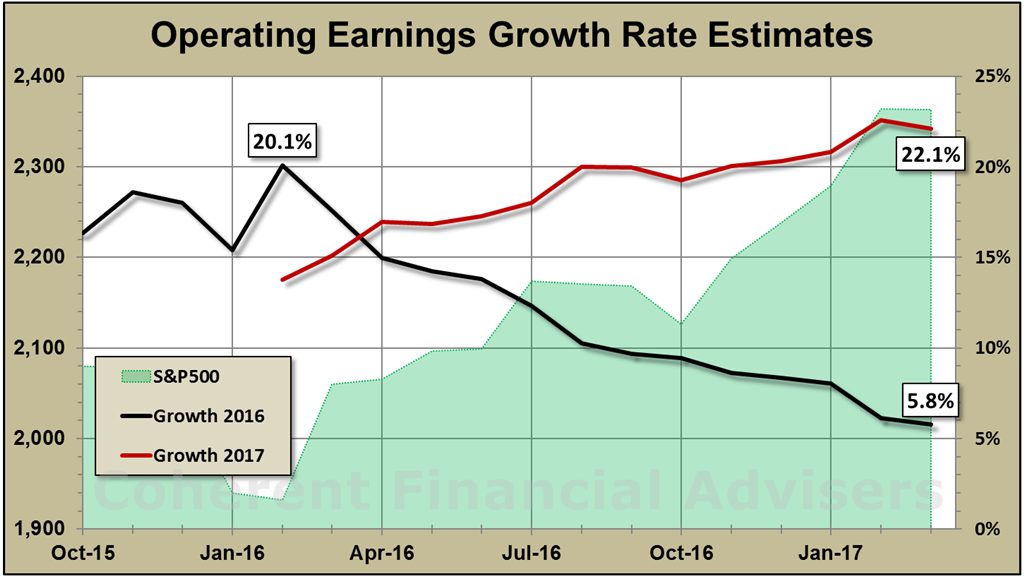

We’ve exceeded 20% earnings growth before, especially after slower growth periods. Our silver-lining-tailwind effect of relatively easy comparable EPS growth is ebbing as trailing earnings become increasingly difficult to beat. Is the necessary sales growth or margins expansion achievable? The second chart helps answer this.

Expectations

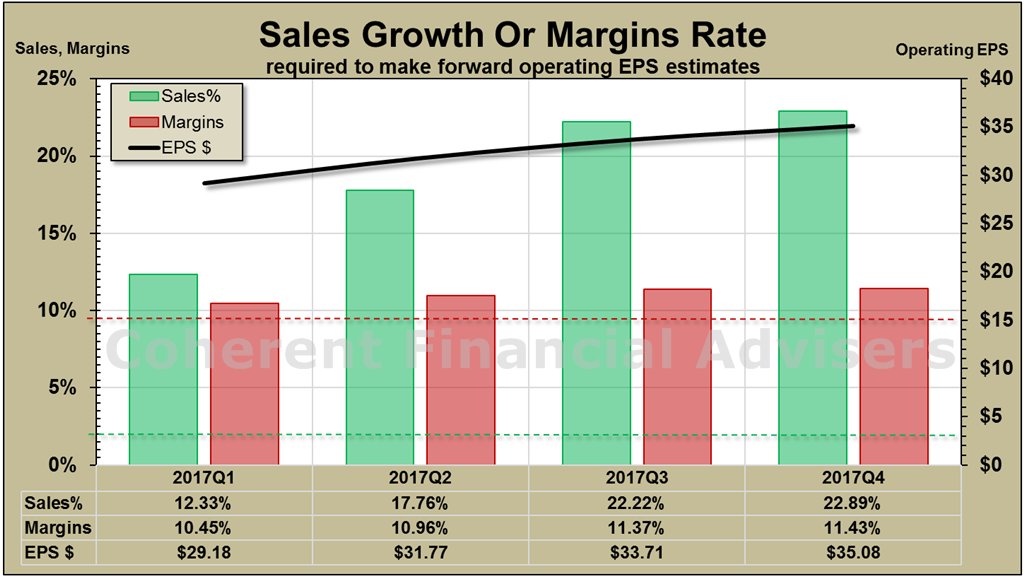

Let’s assume sales growth remains at its 4-year average of 2% (green line). Margins (red bars) must expand to 11%, a millennium record. What if margins rise to their 4-year average of 9.5% (red line)? Then sales (green bars) must grow on average 19% over 2016. More likely is 5% sales growth at 10% margins producing 13% earnings growth. This beats the pants off 2016’s 5% growth, albeit still optimistic. And there’s that pesky 18-PE.

Helena heals the King who rewards her a choice of husband from among his wards. She chooses the man she loves, her original motive for treating the King. The plot thickens, but all’s well in the end. Like Shakespeare, the markets are human nature on display, though they seldom end well – should expectations fail.

Warm regards,

Sargon Zia, CFA

April 3, 2017

You are welcome to comment!

Recommended Reading:

Earnings Insight February 2017

Manager’s Letter 2016 Q4

…other Manager’s Letters

Published quarterly, the Manager’s Letter series primarily communicates the author and Chief Investment Officer’s personal opinion on the markets and other topics of interest to our clients.