Manager’s Letter 2016 Q1

A long-distance trip on a straight highway can be painfully boring without the occasional curve to provide a better view of what’s up ahead. As for markets, I prefer boring. But studying the nature of price swings can yield valuable insight to what might be ahead. The goal is to ascertain whether it’s better to ride out the swings, or take a detour.

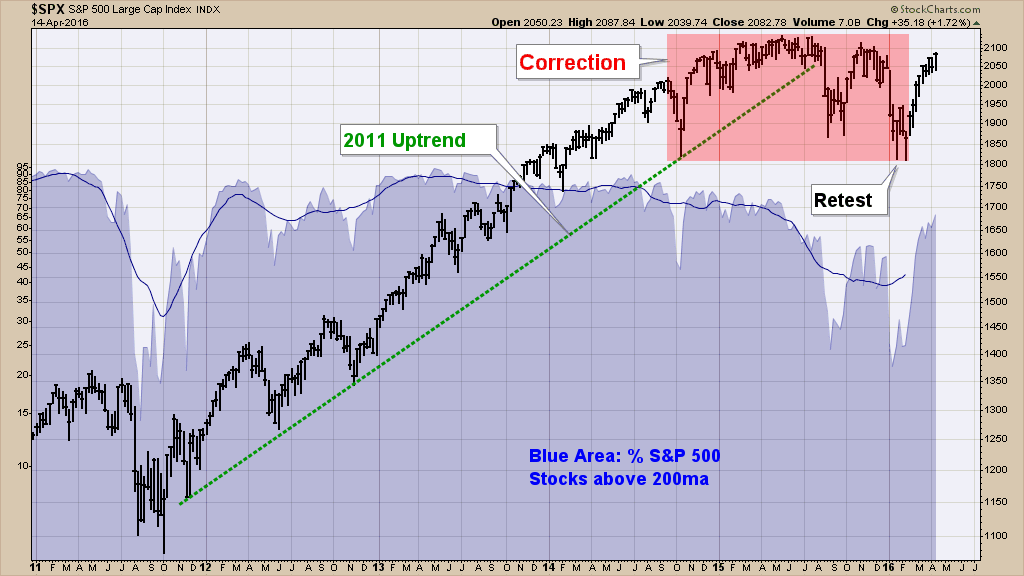

Is The Correction Over?

It has been a tumultuous period since September 2014 when the first crack appeared in the bull market which started in 2011. One year later, the August 2015 tremors would confirm a market that had topped and was correcting. The January aftershocks squelched any remaining euphoria evident in the preceding October rally.

This February’s retest of the August lows begged the question, “Is the September 2014 correction over?” For answers, we continually study both the market’s fundamental health and price behavior. The preponderance of the evidence is seldom beyond a reasonable doubt, compelling us to move cautiously, checking our blind spots.

A Silver Lining For 2016

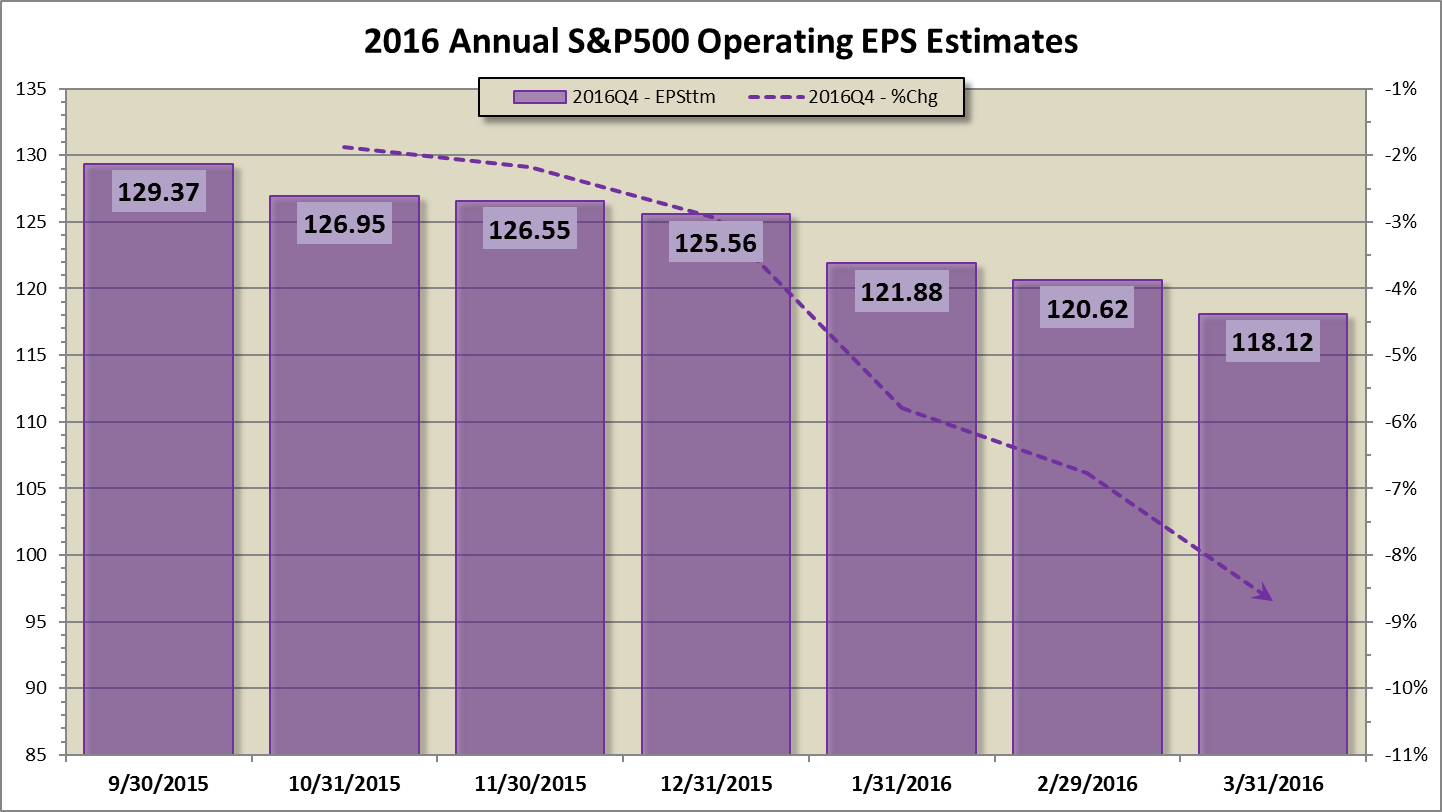

In our Earnings Insight March 2016 article we introduced a “silver lining for 2016”, namely that 2015 earnings contraction has set a low bar for 2016 growth. However, market valuations are still high by historical standards, even if we accept the more optimistic growth estimates. Meanwhile, hopes for 2016 full year revenue and earnings continue to ebb. First quarter S&P 500 Index revenue is expected to contract, marking five consecutive negative quarters, while earnings estimates call for the worst quarter of consecutive contraction since 2015.

When we opted to take a detour last summer by raising cash, our focus turned to determining when and where to get back onto the main road. In our Market Update February 2016 article we indicated that we had started gradually returning to full equity allocation. As earnings season begins, we remain just shy of full equity allocation, but frankly not without some reservations. Individual stock participation has improved since the February bottom and the S&P 500 has broken initial resistance. The veracity of this upswing will depend on forward looking estimates for a possible return to growth in the second half. This market has been habitually over-optimistic.

We encourage you to visit our website where we regularly share our thoughts in current and relevant articles. You can access your accounts from the Client-Tools drop-down. Your connection to our website is private and encrypted at all times using SSL security. We invite you also to connect with us on Facebook, LinkedIn, and Google+, for which you will find links on this page.

Warm regards,

Sargon Zia, CFA

April 14, 2016

You are welcome to comment!

Published quarterly, the Manager’s Letter series primarily communicates the author and Chief Investment Officer’s personal opinion on the markets and other topics of interest to our clients.